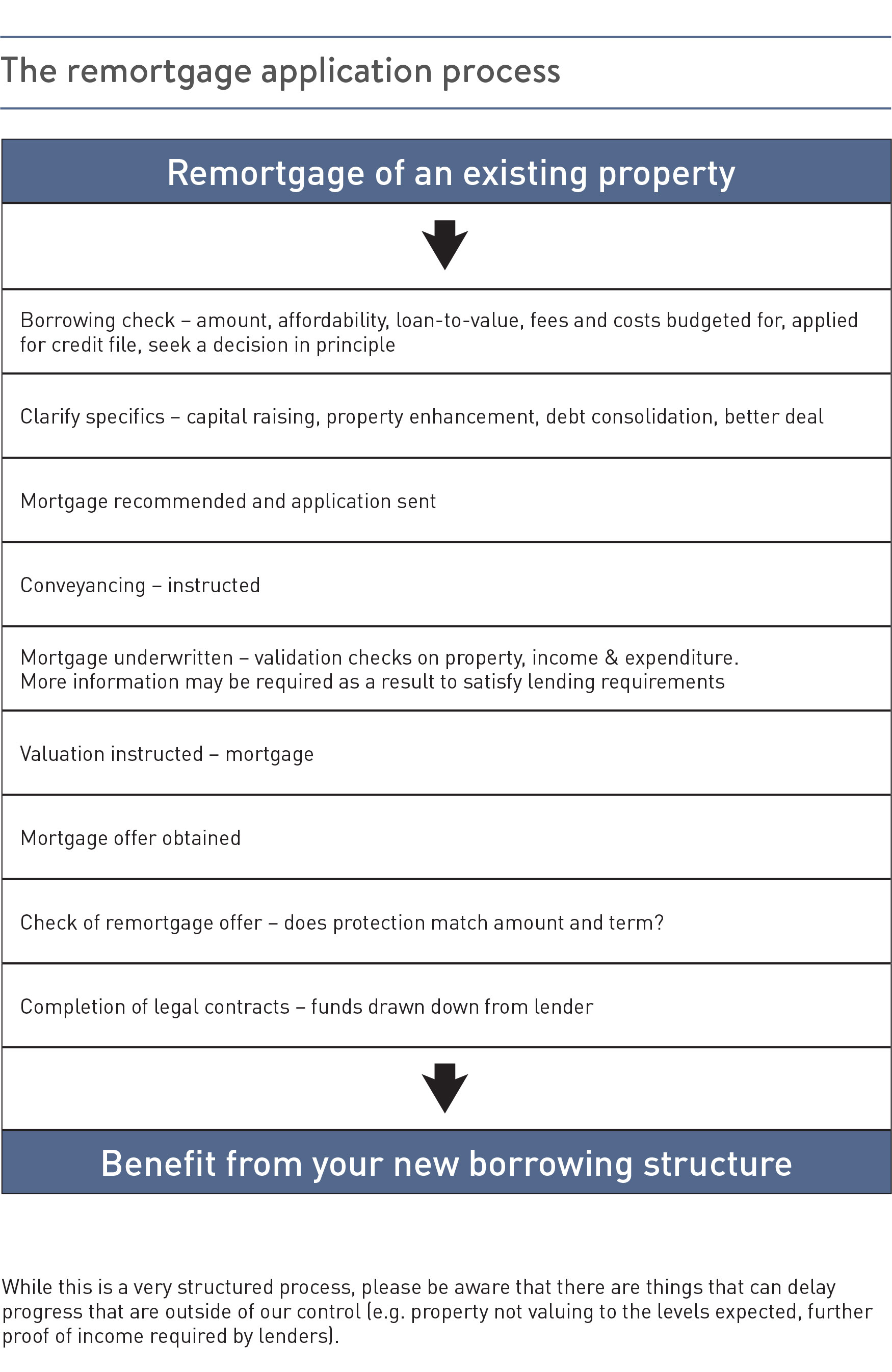

Remortgaging can help your financial health in many ways. In simple terms, remortgaging involves moving your current mortgage to a new arrangement, arranged either with your existing lender or with a new lender.

It is very similar to the home buying process. That said, as it is not something that you do every day so it is important to ensure you have a clear understanding of the process and your knowledge is up-to-date.

This guide will help to clarify the terminology, benefits, risks and associated costs of remortgaging your property.

Here to help you

There are many questions you will need to ask yourself:

- Is it worth doing?

- How much will setting it up cost?

- Can I afford it?

- How will it impact my other borrowing?

- Can I change the type of mortgage?

- Can I go elsewhere or do I have to stay with my current lender?

- Will any employment changes affect this?

The remortgage market is complex. There are many different mortgages to choose from.

So it’s good to know that, as your adviser, we are on hand to answer your questions. We will help you with the tricky process of not only getting a mortgage, but getting the right mortgage.

We take pride in offering a personal service that takes into account your individual circumstances. Your financial situation is unique, so we work hard to understand your goals and aspirations, and make financial recommendations based on a comprehensive and detailed analysis of your needs.

Our role is to:

- ensure you do not waste money unnecessarily by paying a higher monthly amount than you need to for your borrowings

- save you time and effort by choosing the most appropriate solution

- stop you missing out on the most cost effective way of arranging your loan.

Why remortgage?

Many borrowers choose to review their mortgage every few years in order to take advantage of the new rates on offer. Those that remain on the same deal for the full term of their loan could lose out by paying more money than they need to. They could also miss out on the chance to finish their mortgage term earlier than originally planned.

The core reasons to consider remortgaging are:

To avoid moving home

It can be more convenient and cost effective to enhance your existing property, rather than move home. This can be financed by remortgaging or a further advance.

To not lose money unnecessarily

When you took out your current loan, there will have been features that made it competitive and attractive to you. It may be that your incentive period is coming to an end, or simply that the market has changed.

This could allow you to save money on your monthly repayments, or to repay your mortgage sooner. If your current lender doesn’t offer better rates or greater flexibility on its other products, you may want to consider switching your mortgage to another lender. You may be better off doing so, even if this triggers early repayment charges payable to your existing lender, as this could still mean a net saving to you.

To get a lump sum for a special cause

You may have a wedding or education fees to fund. If your property value has risen, you could release some of the equity to help towards this.

To consolidate debts

Remortgaging can allow you to release some of the value you hold in your home and consolidate other debts that can attract higher rates of interest than that of your mortgage (e.g. credit cards).

Think carefully before securing other debts against your home. While debt consolidation often reduces the amount of repayments, making them more affordable, it will normally involve extending the term over which you repay the debt(s), which often results in you paying more for the debt in total.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

CONTACT US

This communication does not constitute advice and should not be taken as a recommendation to purchase any of the products or services mentioned.

Before taking any decisions we suggest you seek professional advice.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY OTHER DEBT SECURED ON IT.